Planning for retirement is one of the most crucial financial decisions you’ll make in your lifetime. At the heart of this planning process lies the choice of the best retirement accounts to secure your financial future.

Whether you’re just starting your career or nearing retirement age, understanding and utilizing the right retirement accounts can make a significant difference in your golden years. This comprehensive guide will walk you through the landscape of the best retirement accounts, helping you make informed decisions to maximize your nest egg.

Skale Money Key Takeaways

- Retirement accounts offer tax advantages that can significantly boost your savings over time

- Employer-sponsored plans like 401(k)s often come with matching contributions, essentially providing free money for your retirement

- Individual Retirement Accounts (IRAs) offer flexibility and control over your investments

- Self-employed individuals have access to powerful retirement savings tools like Solo 401(k)s and SEP IRAs

- Balancing multiple retirement accounts can optimize your savings strategy

- Understanding Required Minimum Distributions (RMDs) is crucial for long-term planning

- Social Security should be considered as part of your overall retirement strategy

Table of Contents

Understanding Retirement Accounts: The Basics

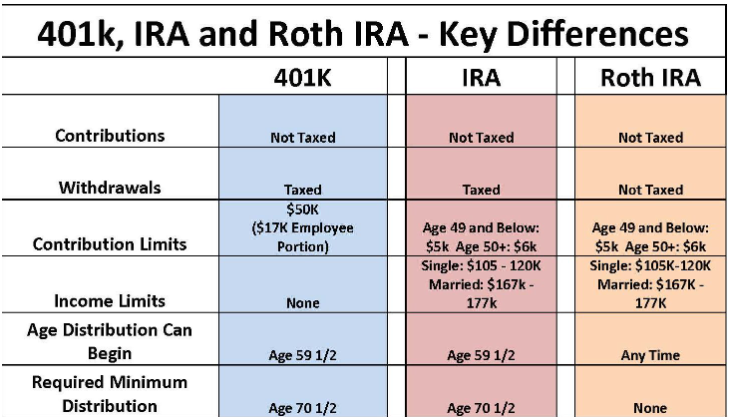

Retirement accounts are specialized financial tools designed to help individuals save and invest for their future. These accounts typically offer tax advantages to incentivize long-term savings.

Types of retirement accounts include:

- Employer-sponsored accounts (e.g., 401(k)s, 403(b)s)

- Individual retirement accounts (IRAs)

- Government pension plans

Here’s a basic comparison of these account types:

| Account Type | Sponsorship | Tax Advantages | Contribution Limits (2024) |

| 401(k) | Employer | Tax-deferred | $23,000 ($30,500 if 50+) |

| Traditional IRA | Individual | Tax-deferred | $7,000 ($8,000 if 50+) |

| Roth IRA | Individual | Tax-free growth | $7,000 ($8,000 if 50+) |

The Power of Tax-Advantaged Accounts

One of the key benefits of the best retirement accounts is their tax-advantaged status. This feature can significantly boost your savings over time.

Tax advantages of retirement accounts include:

- Tax-deferred growth: Your investments grow without being taxed until withdrawal

- Tax-free withdrawals: Some accounts, like Roth IRAs, offer tax-free withdrawals in retirement

- Potential tax deductions: Contributions to certain accounts may lower your current taxable income

Advice: Maximize your tax benefits by contributing to both tax-deferred and tax-free accounts when possible. This strategy, known as tax diversification, can provide flexibility in retirement.

Top Employer-Sponsored Retirement Accounts

Employer-sponsored retirement accounts are often the first stop in building your retirement savings. These plans are typically easy to set up and may come with additional benefits like employer matching.

Let’s explore some of the best retirement accounts offered by employers:

401(k) Plans

401(k) plans are the most common type of employer-sponsored retirement account. They allow you to contribute pre-tax dollars from your paycheck directly into an investment account.

403(b) Plans

Similar to 401(k)s, 403(b) plans are typically offered by public schools and certain non-profit organizations.

457(b) Plans

These plans are usually available to state and local government employees and some non-profit workers.

Thrift Savings Plan (TSP)

The TSP is a retirement savings plan for federal employees and members of the uniformed services.

| Plan Type | Eligible Employees | 2024 Contribution Limit | Catch-Up Contributions (50+) |

| 401(k) | Private sector | $23,000 | $7,500 |

| 403(b) | Public schools, non-profits | $23,000 | $7,500 |

| 457(b) | Government, some non-profits | $23,000 | $7,500 |

| TSP | Federal employees | $23,000 | $7,500 |

Advice: Always try to contribute enough to get the full employer match in your 401(k) or similar plan. This is essentially free money for your retirement.

Best Individual Retirement Accounts (IRAs)

Individual Retirement Accounts (IRAs) offer more flexibility and control over your investments compared to employer-sponsored plans.

They’re an excellent option for supplementing your employer plan or as a primary retirement savings vehicle if you don’t have access to a workplace plan.

Let’s dive into the best retirement accounts in the IRA category:

Traditional IRA

- Contributions may be tax-deductible

- Earnings grow tax-deferred

- Withdrawals in retirement are taxed as ordinary income

Roth IRA

- Contributions are made with after-tax dollars

- Earnings grow tax-free

- Qualified withdrawals in retirement are tax-free

SEP IRA

- Designed for self-employed individuals and small business owners

- High contribution limits based on a percentage of income

SIMPLE IRA

- Suitable for small businesses with 100 or fewer employees

- Requires employer contributions

Pros and cons of each IRA type:

- Traditional IRA:

- Pro: Potential for immediate tax deduction

- Con: Required Minimum Distributions (RMDs) at age 73

- Roth IRA:

- Pro: Tax-free withdrawals in retirement

- Con: No immediate tax benefit

- SEP IRA:

- Pro: High contribution limits

- Con: Employer must contribute equally for all eligible employees

- SIMPLE IRA:

- Pro: Easy to set up and maintain

- Con: Lower contribution limits than 401(k)s

Advice: Consider your current tax bracket and expected retirement tax bracket when choosing between Traditional and Roth IRAs. If you expect to be in a higher tax bracket in retirement, a Roth IRA might be more beneficial.

Self-Employed Retirement Accounts

Self-employed individuals have access to some of the best retirement accounts with high contribution limits. These options allow entrepreneurs and freelancers to save aggressively for retirement.

Solo 401(k)

- Combines employee and employer contributions

- High contribution limits: up to $69,000 in 2024 ($76,500 if 50 or older)

SEP IRA (for self-employed)

- Easy to set up and maintain

- Contributions can be up to 25% of net earnings, up to $69,000 in 2024

Defined Benefit Plans

- Allows for very high contributions based on actuarial calculations

- Best for high-income self-employed individuals nearing retirement

| Account Type | 2024 Contribution Limit | Catch-Up Contributions (50+) | Ease of Setup |

| Solo 401(k) | $69,000 | $7,500 | Moderate |

| SEP IRA | $69,000 or 25% of compensation | N/A | Easy |

| Defined Benefit | Based on actuarial calculation | N/A | Complex |

Factors to consider when choosing a self-employed retirement account:

- Your income level and stability

- Desired contribution amount

- Complexity of administration

- Whether you have employees

Strategies for Maximizing Your Retirement Savings

To make the most of the best retirement accounts available to you, consider these strategies:

- Maximize employer matches in 401(k) plans

- Make catch-up contributions if you’re 50 or older

- Diversify across account types (e.g., combine a 401(k) with a Roth IRA)

- Regularly rebalance your portfolio to maintain your desired asset allocation

Advice: Avoid these common mistakes in retirement planning:

- Not starting early enough

- Failing to increase contributions as your income grows

- Overlooking fees in your investment choices

- Borrowing from your retirement accounts

Navigating Required Minimum Distributions (RMDs)

Understanding RMDs is crucial when managing the best retirement accounts, as they can impact your tax situation in retirement.

Key RMD rules:

- RMDs generally begin at age 73 (as of 2024)

- First RMD must be taken by April 1 of the year following the year you turn 73

- Subsequent RMDs must be taken by December 31 each year

- Failure to take RMDs results in a 25% penalty on the amount not withdrawn

| Account Type | RMD Required? | RMD Start Age |

| Traditional IRA | Yes | 73 |

| 401(k) | Yes* | 73 |

| Roth IRA | No | N/A |

| Roth 401(k) | Yes** | 73 |

* Unless still working for the employer sponsoring the plan ** Can be avoided by rolling over to a Roth IRA

Advice: Consider Roth conversions in lower-income years to reduce future RMDs and potentially lower your tax burden in retirement.

The Role of Social Security in Retirement Planning

While not typically considered among the best retirement accounts, Social Security plays a crucial role in most Americans’ retirement plans.

Important Social Security considerations:

- Eligibility typically requires 40 quarters of covered employment

- Full retirement age ranges from 66 to 67, depending on birth year

- Benefits can be claimed as early as 62 (with reduced payments) or delayed up to age 70 (with increased payments)

| Claiming Age | % of Full Benefit |

| 62 | 70% |

| Full Retirement Age | 100% |

| 70 | 124% |

Advice: View Social Security as a foundation for your retirement income, but not the sole source. The best retirement accounts should be used to build upon this foundation.

Balancing Multiple Retirement Accounts

Many individuals find themselves with multiple retirement accounts over the course of their careers. Balancing these can be key to optimizing your retirement strategy.

Strategies for managing multiple accounts:

- Prioritize contributions to accounts with employer matching

- Consider tax diversification across accounts

- Aim for a coherent overall asset allocation across all accounts

Advice: Regularly review your accounts to ensure they align with your overall retirement strategy. Consider consolidating accounts if it simplifies management without sacrificing benefits.

Conclusion

Choosing and maximizing the best retirement accounts is a crucial step in securing your financial future. From employer-sponsored 401(k)s to individual IRAs and specialized accounts for the self-employed, each option offers unique benefits.

By understanding these accounts, taking advantage of tax benefits, and employing smart saving strategies, you can build a robust retirement nest egg.

Remember, the ideal retirement savings strategy is personal and depends on your individual circumstances, including your age, income, employment situation, and retirement goals. Regular review and adjustment of your retirement accounts can help ensure you’re on track for the retirement you envision.

Start early, save consistently, and make informed decisions about the best retirement accounts for your situation. Your future self will thank you for the effort you put in today.

Frequently Asked Questions (FAQ)

What is the best retirement account for most people?

For most employees, a 401(k) with employer matching is an excellent starting point. Combining this with a Roth IRA can provide tax diversification.

How much should I contribute to my retirement accounts?

Aim to save at least 15% of your income for retirement, including any employer contributions. If possible, max out your contributions to the best retirement accounts available to you.

Can I contribute to both a 401(k) and an IRA?

Yes, you can contribute to both. However, if you’re covered by a workplace retirement plan, your ability to deduct traditional IRA contributions may be limited based on your income.

What’s the difference between a traditional and Roth IRA?

Traditional IRAs offer tax-deductible contributions and tax-deferred growth, with taxes paid on withdrawals. Roth IRAs use after-tax dollars but offer tax-free growth and withdrawals in retirement.

How do I choose between a traditional and Roth 401(k)?

Consider your current tax bracket and expected retirement tax bracket. If you expect to be in a higher tax bracket in retirement, a Roth 401(k) might be more beneficial.

What happens to my 401(k) if I change jobs?

You typically have several options: leave it with your former employer, roll it over to your new employer’s plan, roll it over to an IRA, or cash it out (which is generally not recommended due to taxes and penalties).

Are there any retirement accounts for stay-at-home parents?

Yes, a spousal IRA allows a working spouse to contribute to an IRA for a non-working spouse, providing retirement savings opportunities for stay-at-home parents.

Author: Cosmas Mwirigi

Cosmas Mwirigi is an established freelance writer with over five years of experience and the founder of Skalemoney.com. Cosmas Mwirigi has been published on PV-Magazine, Slidebean, Bridge Global, Casinos.com, Gambling.com, and Reverbico among many other websites.

Cosmas Mwirigi is an expert writer in iGaming, B2B, SaaS, Finance, digital marketing and Solar renewable energy. To contact him for his services, connect with him on his LinkedIn

![]()