Your ability to earn an income is arguably your most valuable financial asset. Yet, many people overlook the importance of protecting this asset through disability insurance options.

According to the Social Security Administration, more than one in four of today’s 20-year-olds will experience a disability before reaching retirement age. This comprehensive guide will walk you through everything you need to know about disability insurance options, helping you make an informed decision about protecting your financial future.

Skale Money Key Takeaways

- Disability insurance options come in various forms, including short-term, long-term, individual, and group coverage

- The right disability insurance choice depends on your occupation, income level, and personal circumstances

- Employer-provided coverage often needs supplementation with individual disability insurance

- Policy features and riders can significantly impact the value of your disability coverage

- Understanding the claims process before purchasing is crucial for maximum benefit utilization

- Industry-specific options exist for specialized professions

- Cost considerations should balance premium affordability with adequate coverage

Table of Contents

1. Understanding Disability Insurance Options: The Fundamentals

Disability insurance serves as a financial safety net when you’re unable to work due to illness or injury. Understanding the basic types of coverage is essential for making an informed decision about your protection needs.

Different types of disability insurance options include:

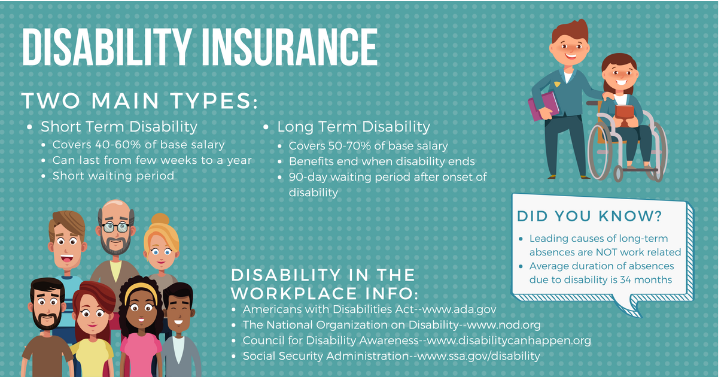

- Short-term disability insurance: Covers 3-6 months with benefits starting almost immediately

- Long-term disability insurance: Provides coverage for several years or until retirement

- Individual disability insurance: Purchased privately, offering customizable coverage

- Group disability insurance: Provided through employers with standardized benefits

| Type | Benefit Duration | Waiting Period | Typical Coverage Amount |

| Short-term | 3-6 months | 0-14 days | 60-70% of income |

| Long-term | To retirement | 90-180 days | 60-80% of income |

| Individual | Varies | Customizable | Up to 70% of income |

| Group | Varies | Set by employer | 50-60% of income |

2. How to Assess Your Disability Insurance Needs

Before exploring specific disability insurance options, it’s crucial to evaluate your personal needs and circumstances. This assessment will help determine the appropriate coverage level and type for your situation.

Consider these key factors:

- Current monthly expenses and financial obligations

- Emergency savings and other financial resources

- Number of dependents and their needs

- Career stage and future earning potential

- Existing coverage through employer or other sources

Assessment Checklist:

- Calculate monthly living expenses

- Review current savings and assets

- Evaluate existing coverage

- Consider career-specific risks

- Assess long-term financial goals

3. Employer-Provided vs. Individual Disability Insurance Options

Understanding the differences between employer-provided and individual disability insurance options is crucial for creating comprehensive coverage.

| Feature | Employer-Provided | Individual |

| Portability | Typically ends with employment | Stays with you regardless of job |

| Cost | Often employer-subsidized | Higher premiums but tax advantages |

| Customization | Limited options | Highly customizable |

| Coverage Amount | Usually capped | Can be tailored to needs |

| Definition of Disability | Often stricter | More flexible options |

Recommendations based on common scenarios:

- Young professionals: Combine employer coverage with supplemental individual policy

- Self-employed: Focus on comprehensive individual coverage

- High-income earners: Layer multiple policies for adequate protection

- Career changers: Prioritize portable individual coverage

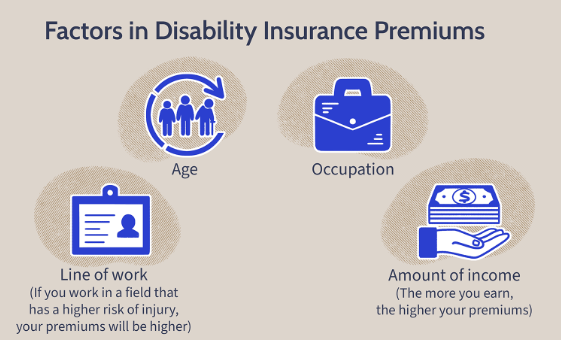

4. Cost Factors and Premium Considerations

Understanding what influences disability insurance premiums helps in budgeting and selecting appropriate coverage levels.

Primary factors affecting premium costs:

- Age at policy purchase

- Occupation risk level

- Health status and medical history

- Coverage amount and benefit period

- Policy features and riders selected

Tips for managing premium costs:

- Purchase early when rates are lower

- Choose a longer elimination period

- Select only necessary riders

- Maintain good health

- Consider group association discounts

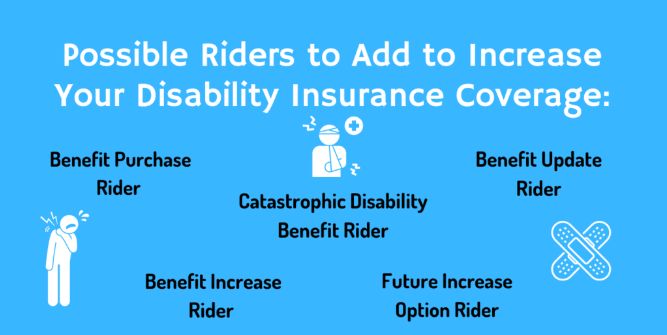

5. Essential Policy Features and Riders

An effective disability insurance policy often requires customization through various features and riders to match your specific needs.

Essential features to consider:

- Own-occupation coverage

- Residual disability benefits

- Cost-of-living adjustments

- Future increase options

- Recovery benefits

| Rider | Purpose | Typical Cost Impact |

| COLA | Protects against inflation | 10-15% increase |

| Future Increase | Allows coverage increases | 5-10% increase |

| Residual | Partial disability coverage | 10-20% increase |

| Student Loan | Additional benefits for loans | 15-25% increase |

6. Industry-Specific Disability Insurance Options

Different professions have unique income protection needs, leading to specialized disability insurance options.

Industry-specific considerations:

- Medical Professionals:

- High-income protection needs

- Specialty-specific coverage

- Student loan protection

- Legal Professionals:

- Partnership protection

- Buy-sell agreement funding

- High-income coverage

- Business Owners:

- Business overhead expense coverage

- Key person protection

- Multiple policy coordination

- Skilled Trades:

- Occupation-specific definitions

- Physical disability focus

- Return-to-work programs

7. Application Process and Underwriting

The application process for disability insurance options involves several steps and requirements.

Required documentation:

- Income verification (tax returns, W-2s)

- Medical history and records

- Occupation details and duties

- Financial obligations

- Existing coverage information

Timeline expectations:

- Initial application (1-2 days)

- Medical exam scheduling (3-5 days)

- Records collection (2-4 weeks)

- Underwriting review (1-2 weeks)

- Policy approval and delivery (1 week)

8. Claims Process and Benefits Distribution

Understanding the claims process ensures you can access benefits when needed.

Essential claims documentation:

- Physician’s statement

- Employer verification

- Detailed symptoms and limitations

- Treatment records

- Financial documentation

Tips for successful claims:

- Report claims promptly

- Maintain detailed records

- Follow treatment plans

- Stay in communication

- Consider professional assistance

9. Future of Disability Insurance Options

The disability insurance landscape continues to evolve with technological advances and changing workforce needs.

Emerging trends:

- Digital application processes

- Simplified underwriting

- Flexible coverage options

- Integration with wellness programs

- Enhanced return-to-work support

Conclusion

Selecting the right disability insurance options requires careful consideration of your personal circumstances, career trajectory, and financial needs.

By understanding the various types of coverage, policy features, and application processes, you can make an informed decision about protecting your income. Remember that the best disability insurance policy is the one that provides adequate coverage when you need it most.

Frequently Asked Questions

What’s the difference between own-occupation and any-occupation disability insurance?

Own-occupation coverage pays benefits if you can’t perform your specific occupation, while any-occupation coverage only pays if you can’t work in any job suitable for your education and experience.

How much disability insurance coverage do I need?

Generally, aim to cover 60-70% of your gross income, considering your monthly expenses, savings, and other sources of income.

Can I have multiple disability insurance policies?

Yes, you can have multiple policies, but insurance companies typically limit total coverage to 70-75% of your income.

What medical conditions qualify for disability insurance?

Qualifying conditions vary by policy but typically include physical injuries, mental health conditions, chronic illnesses, and cognitive impairments.

How long does disability insurance coverage last?

Coverage duration depends on the policy type, ranging from a few months for short-term disability to retirement age for long-term disability.

What’s not covered by disability insurance?

Common exclusions include pre-existing conditions, self-inflicted injuries, criminal activities, and disabilities occurring during military service.

Additional Resources

- Social Security Administration Disability Resources

- State Insurance Department Guidelines

- Professional Association Insurance Programs

- Financial Planning Calculators

- Insurance Terminology Glossary

![]()