When it comes to setting financial goals, we’ve all been there – enthusiastically writing down ambitious targets on New Year’s Eve, only to find ourselves off track by February.

The statistics are sobering: 92% of financial resolutions fail, leaving many wondering what sets the successful 8% apart. This isn’t just about willpower or knowledge; it’s about understanding the intricate psychology behind our financial behaviors and learning how to work with our minds rather than against them.

In this comprehensive guide, we’ll explore the psychological principles that influence our financial decisions and provide you with actionable strategies to join the successful minority who achieve their monetary aspirations.

Skale Money Key Takeaways

Before diving deep into the psychology of setting financial goals, here are the essential insights you’ll gain from this article:

- Understanding the psychological barriers that prevent financial success

- Learning research-backed strategies for effective goal setting

- Discovering practical implementation techniques that work with your brain, not against it

- Mastering the art of building sustainable financial habits

- Developing resilience against common setbacks

Table of Contents

Understanding the Psychology of Financial Behavior

Our relationship with money is deeply rooted in psychological patterns that often operate beneath our conscious awareness. Behavioral economics has revealed several key barriers that impact our financial decision-making process.

These psychological obstacles include:

- Loss aversion: We feel the pain of losses twice as intensely as the pleasure of gains

- Present bias: The tendency to prioritize immediate rewards over long-term benefits

- Choice paralysis: Becoming overwhelmed by too many financial options

- Mental accounting: Treating money differently based on its source or intended use

- Status quo bias: Sticking with current financial situations even when better alternatives exist

The Science Behind Goal Setting and Money Management

The intersection of neuroscience and financial planning reveals fascinating insights into how our brains process monetary decisions. Research shows that financial planning activates the same neural pathways as other forms of future-oriented thinking.

Recent studies have uncovered several critical findings:

- Stress directly impacts our financial decision-making abilities by reducing activity in the prefrontal cortex

- Dopamine release patterns influence our saving and spending habits

- Emotional states can override logical financial planning

- Social comparison significantly affects our spending patterns and financial satisfaction

Common Reasons Financial Goals Fail

Understanding why financial goals typically fail is crucial for setting yourself up for success. The most common pitfalls often stem from psychological rather than practical limitations.

Key failure points include:

- Setting unrealistic expectations without considering psychological readiness

- Failing to establish specific, measurable objectives

- Lacking accountability systems and support structures

- Maintaining environments filled with spending triggers

- Experiencing decision fatigue from overly complex financial plans

- Succumbing to emotional spending triggers without coping mechanisms

The 8% Success Formula: What Sets Them Apart

The small percentage who succeed in setting financial goals and achieving them share several distinctive characteristics. Their approach to financial planning integrates both practical and psychological elements.

Success factors common among the 8% include:

- Maintaining crystal clear purpose and vision

- Implementing systems rather than relying solely on willpower

- Utilizing robust progress tracking methods

- Building and maintaining strong support networks

- Developing comprehensive contingency plans for setbacks

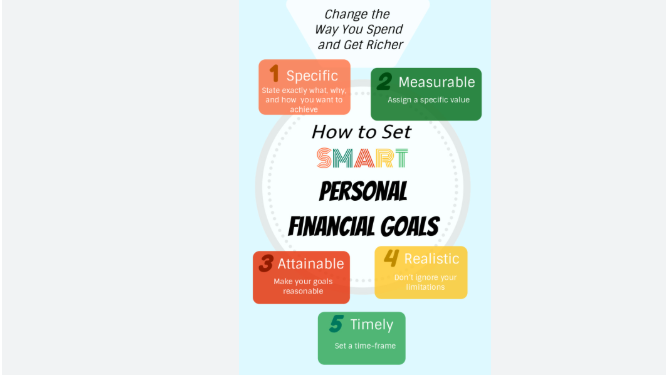

Creating Psychology-Backed Financial Goals

The SMART+ framework builds upon traditional goal-setting methods by incorporating psychological elements essential for financial success.

Table: Goal-Setting Framework Template

| Component | Questions to Ask | Example |

| Specific | What exactly do I want? | Save $10,000 |

| Measurable | How will I track progress? | Monthly savings of $833 |

| Achievable | Is this realistic for me? | Based on 15% of income |

| Relevant | Why does this matter? | Emergency fund security |

| Time-bound | When will I achieve this? | 12 months |

| Emotional | How does this align with my values? | Family security |

When setting financial goals, each component must be carefully considered and personalized to your situation. The emotional alignment aspect is particularly crucial as it helps maintain motivation during challenging periods.

Implementation Strategies That Work

Turning financial goals into reality requires practical implementation strategies that account for human psychology. Success lies in creating systems that make it easier to maintain positive financial behaviors.

Effective action steps include:

- Designing your environment to support financial goals (e.g., removing shopping apps)

- Stacking new financial habits onto existing routines

- Automating key financial behaviors where possible

- Using visual progress tracking tools

- Establishing accountability partnerships with clear check-in protocols

Overcoming Psychological Barriers

Even with well-designed goals and implementation strategies, psychological barriers can derail your financial progress. Developing specific techniques to overcome these obstacles is essential.

The strategy toolkit should include:

- Cognitive restructuring techniques for challenging limiting money beliefs

- Emotional regulation methods for managing financial stress

- Mindfulness practices for conscious spending decisions

- Social support utilization strategies

- Stress management approaches specifically for financial challenges

Maintaining Long-Term Financial Success

Achieving financial goals is only half the battle; maintaining success requires a different set of psychological tools and approaches.

Key factors for long-term success include:

- Regular review and adjustment processes

- Meaningful celebration of financial milestones

- Flexible course correction strategies

- Development of positive financial identity

- Cultivation of growth mindset regarding money

Building Resilience Against Financial Setbacks

Financial setbacks are inevitable, but resilience determines whether they become permanent failures or temporary obstacles.

Essential elements of the resilience toolkit include:

- Comprehensive emergency planning protocols

- Flexible goal adjustment strategies

- Specific recovery procedures for common setbacks

- Methods for extracting lessons from financial mistakes

- Systems for activating support networks during challenges

Conclusion

Setting financial goals successfully requires more than just numbers and spreadsheets – it demands a deep understanding of your psychological relationship with money.

By implementing the strategies outlined in this guide and working with, rather than against, your brain’s natural tendencies, you can join the 8% who achieve their financial objectives.

Remember that success in setting financial goals isn’t about perfection but progress.

Start with small, manageable changes that align with your psychological preferences and gradually build upon your successes. The path to financial achievement begins with understanding yourself and creating systems that support your natural tendencies rather than fight against them.

Frequently Asked Questions

How long does it take to form a financial habit?

Research suggests that while the traditional 21-day rule is a myth, most people require 66 days to form a stable financial habit. However, this can vary significantly based on individual circumstances and the complexity of the habit.

What if I’ve failed at financial goals before?

Past failures often provide valuable insights for future success. Use previous experiences to identify specific triggers and obstacles, then adjust your approach accordingly. Remember that each attempt brings you closer to understanding what works for you.

How do I stay motivated during setbacks?

Maintain motivation by connecting with your core financial values, celebrating small wins, and utilizing your support network. Having a clear “why” behind your financial goals helps sustain momentum during challenging periods.

Should I share my financial goals with others?

Selective sharing can be beneficial. Choose accountability partners who support your goals and understand your challenges. However, be mindful that some people might unintentionally undermine your progress through their own financial anxieties.

How often should I review my financial goals?

Establish a regular review schedule – monthly for checking progress, quarterly for minor adjustments, and annually for major revisions. This helps maintain focus while allowing flexibility for changing circumstances.

What role does automation play in goal success?

Automation reduces the cognitive load of financial decisions and helps bypass psychological barriers. However, it should be balanced with conscious awareness of your financial situation to maintain engagement with your goals.

This comprehensive approach to setting financial goals, grounded in psychological research and practical application, provides the framework needed to join the successful 8%. Remember that financial success is a journey, not a destination, and each step forward, no matter how small, brings you closer to your goals.

![]()