A credit score serves as a numerical representation of your creditworthiness, influencing lenders’ decisions on whether to approve your loan application.

This blog post aims to explore the importance of the credit score definition in loan approval processes, shedding light on how it affects your financial opportunities.

Skale Money Key Takeaway

- Understanding the definition of a credit score is vital for anyone seeking loans.

- It influences not only approval chances but also the terms and interest rates offered by lenders.

- Maintaining a good credit score through responsible financial practices can open doors to better borrowing options.

Table of Contents

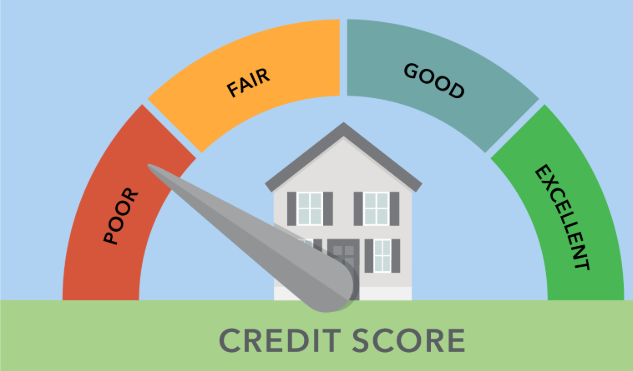

1. What is a Credit Score?

A credit score is a three-digit number that summarizes your credit history and indicates how likely you are to repay borrowed money. Ranging from 300 to 850, a higher score signifies better creditworthiness. Various scoring models exist, with FICO and VantageScore being the most commonly used by lenders.

Key Points:

- Numerical Representation: Your credit score reflects your credit risk.

- Score Range: Scores typically range from 300 (poor) to 850 (excellent).

- Scoring Models: Different lenders may use different scoring models.

Table: Credit Score Ranges and Classifications

| Score Range | Classification | Implications |

| 300-579 | Poor | High risk, likely loan denial |

| 580-669 | Fair | Higher interest rates |

| 670-739 | Good | Favorable loan terms |

| 740-799 | Very Good | Low interest rates |

| 800-850 | Excellent | Best loan offers |

2. How Credit Scores Are Calculated

Credit scores are calculated based on several factors that reflect your financial behavior. Understanding these components can help you manage and improve your score effectively.

Key Points:

- Payment History (35%): Timely payments boost your score.

- Credit Utilization (30%): Keeping balances low relative to credit limits is essential.

- Length of Credit History (15%): A longer history can positively impact your score.

- Types of Credit (10%): A mix of credit types (credit cards, loans) can be beneficial.

- New Credit Inquiries (10%): Too many inquiries in a short time can hurt your score.

Advice:

To maintain a healthy credit score, focus on making payments on time, reducing outstanding debts, and keeping your credit utilization below 30%.

3. The Role of Credit Scores in Loan Approval

Lenders utilize credit scores as a quick assessment tool to gauge the risk associated with lending money. A strong credit score can significantly enhance your chances of loan approval.

Key Points:

- Risk Assessment: Lenders rely on scores to determine the likelihood of repayment.

- Loan Approval Rates: Higher scores correlate with higher approval rates.

- Types of Loans Affected: Mortgages, personal loans, and auto loans are all influenced by credit scores.

4. Impact of Credit Score on Interest Rates

Your credit score not only affects whether you get approved for a loan but also the interest rates you’ll be offered. Higher scores typically lead to lower rates, which can save you significant amounts over time.

Key Points:

- Lower Rates for Higher Scores: A good credit score can qualify you for better interest rates.

- Example Scenarios: Understanding how different scores affect monthly payments can illustrate this impact.

Table: Interest Rates Based on Credit Score Ranges

| Credit Score Range | Interest Rate (%) | Monthly Payment (for $300,000 mortgage) |

| 760-850 | 3.5 | $1,347 |

| 700-759 | 4.0 | $1,432 |

| 640-699 | 4.5 | $1,520 |

| Below 640 | 5.0 | $1,610 |

5. Common Misconceptions About Credit Scores

There are many myths surrounding credit scores that can lead to confusion and poor financial decisions. Clarifying these misconceptions is essential for effective financial management.

Key Points:

- Myth: Checking your own credit score lowers it.

- Myth: Closing old accounts improves your score.

- Myth: All lenders use the same scoring model.

6. Steps to Improve Your Credit Score

Improving your credit score is an achievable goal that requires consistent effort and informed strategies.

Key Points:

- Pay Bills on Time: Set reminders or automate payments to avoid late fees.

- Reduce Outstanding Debts: Focus on paying down high-interest debts first.

- Keep Credit Utilization Low: Aim for below 30% of your total available credit.

Advice:

Regularly check your credit report for errors and dispute any inaccuracies promptly.

7. The Future of Credit Scoring

As technology evolves, so does the landscape of credit scoring. Emerging trends could reshape how lenders evaluate borrowers.

Key Points:

- Alternative Data Sources: Some lenders are beginning to consider non-traditional data (like utility payments) in their assessments.

- Technology and AI Impact: Innovations may lead to more personalized lending experiences based on individual financial behavior.

Conclusion

In conclusion, knowing the importance of the credit score definition in loan approval processes can empower consumers to take control of their financial futures. By actively managing their scores and dispelling common myths, individuals can improve their chances of securing favorable loan terms and interest rates.

FAQ

What is considered a good credit score?

A good credit score typically falls above 700, but this can vary by lender.

How often should I check my credit score?

It is advisable to check your credit score at least once a year.

Can I improve my credit score quickly?

While some improvements can be made quickly by paying down debts, significant changes may take time.

Do all lenders use the same criteria for evaluating my credit score?

No, different lenders may have varying criteria and thresholds for what they consider an acceptable score.

What should I do if my loan application is denied due to my credit score?

Review your credit report for errors, improve your financial habits, and consider seeking advice from a financial counselor before reapplying.

![]()