Imagine standing at the crossroads of your financial future, armed with nothing but a three-digit number that holds the key to your dreams.

Your credit score is more than just a number; it’s a powerful narrative of your financial journey, a story of responsibility, resilience, and potential.

Credit score ranges aren’t just abstract figures; they’re gatekeepers to opportunities, silent judges of your financial health, and ultimately, a roadmap to personal transformation.

This isn’t just another dry financial guide.

It’s a beacon of hope for anyone who’s ever felt overwhelmed by their financial situation. Whether you’re struggling with a low credit score or looking to elevate your financial standing, this journey from zero to hero is about to begin.

Table of Contents

Understanding Credit Score Basics

Credit scores can seem like a mysterious language spoken only by bankers and financial experts. Let’s demystify this world and bring it down to earth.

A credit score is essentially a numerical representation of your creditworthiness, a snapshot of how likely you are to repay borrowed money.

Key points to understand about credit scores:

- Calculated by major credit bureaus (Equifax, Experian, TransUnion)

- Typically ranges from 300 to 850

- Based on multiple financial behaviors

- Updated regularly to reflect your current financial situation

The five main components that shape your credit score include:

- Payment History (35%): Your track record of paying bills on time

- Credit Utilization (30%): How much of your available credit you’re using

- Length of Credit History (15%): How long you’ve been managing credit

- Credit Mix (10%): The variety of credit types you have

- New Credit Inquiries (10%): Recent applications for credit

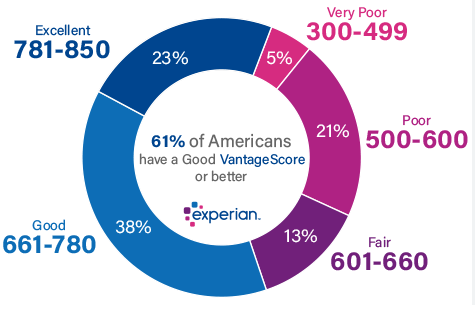

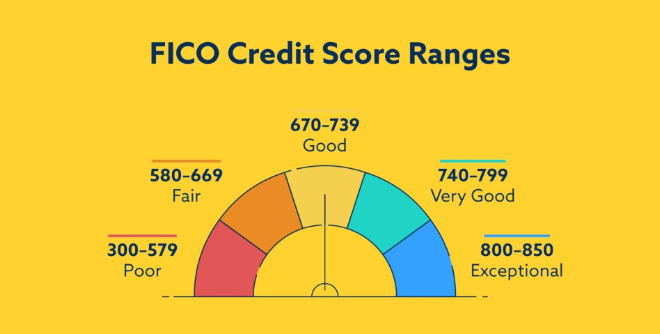

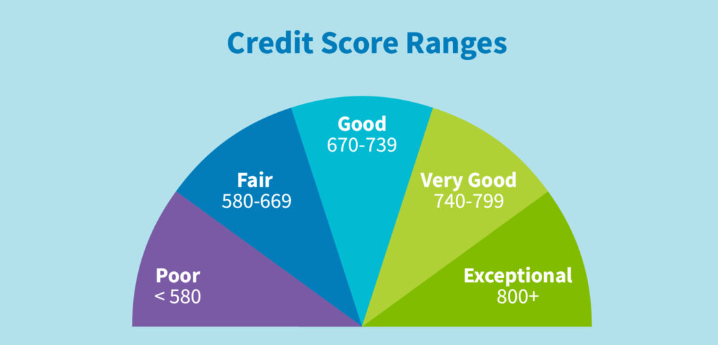

Credit Score Ranges Explained

Understanding credit score ranges is crucial to navigating your financial landscape. Here’s a comprehensive breakdown:

| Range | Classification | Implications |

| 300-579 | Poor | Limited credit options, high-risk borrower |

| 580-669 | Fair | Basic credit access, higher interest rates |

| 670-739 | Good | Moderate credit opportunities, reasonable terms |

| 740-799 | Very Good | Excellent loan terms, lower interest rates |

| 800-850 | Exceptional | Premium financial products, best rates available |

Each range tells a story about your financial health. A poor credit score doesn’t mean you’re a bad person—it’s simply a starting point for improvement.

Those in the good to exceptional ranges enjoy significantly better financial opportunities, lower interest rates, and greater financial flexibility.

The Personal Cost of Low Credit Scores

The impact of low credit score ranges extends far beyond simple numbers. It’s a reality that can touch every aspect of your life:

- Higher interest rates on loans and credit cards

- Difficulty securing housing rentals

- Potential employment challenges

- Limited access to financial products

- Increased personal stress and financial anxiety

Real-world consequences can be profound. A low credit score might mean:

- Paying thousands more in interest over a lifetime

- Being denied an apartment lease

- Struggling to get a car loan

- Facing challenges in starting a business

Strategies for Credit Score Improvement

Transforming your credit score is possible with a strategic approach. Here are proven methods to climb the credit score ranges:

Practical Strategies:

- Pay all bills on time, every time

- Reduce credit card balances

- Keep credit utilization under 30%

- Avoid opening multiple new credit accounts quickly

- Regularly check your credit report for errors

Recommended Action Checklist:

- Set up automatic bill payments

- Create a budget to manage expenses

- Pay down existing debt

- Keep old credit accounts open

- Dispute any incorrect information on credit reports

Credit Repair Myths vs. Reality

Misconceptions about credit scores can be dangerous. Let’s separate fact from fiction:

Myths Debunked:

- Myth: Checking your credit hurts your score

- Reality: Soft inquiries don’t impact your credit

- Myth: You need to carry a balance to build credit

- Reality: Paying balances in full is actually beneficial

- Myth: All debt is bad for your credit

- Reality: Responsible debt management can improve scores

- Myth: Credit repair is an instant process

- Reality: Improving credit takes time and consistent effort

Tools and Resources for Credit Management

Empower yourself with these valuable tools:

- Free credit monitoring services (Credit Karma, Credit Sesame)

- Budgeting apps (YNAB, Mint)

- Credit score tracking applications

- Financial education websites

- Non-profit credit counseling services

Pro Tips:

- Use free annual credit reports

- Take advantage of credit monitoring services

- Invest in financial education resources

- Consider credit counseling if you’re struggling

Long-Term Credit Health Strategies

Building sustainable financial health is a marathon, not a sprint:

- Create and stick to a realistic budget

- Build an emergency fund

- Continue financial education

- Regularly review credit reports

- Plan for major financial milestones

- Diversify your credit mix responsibly

Conclusion

Your financial transformation is a journey of personal growth, resilience, and strategic decision-making. The credit score ranges you see today are not your final destination they’re merely a checkpoint.

With knowledge, discipline, and consistent effort, you can move from zero to hero, unlocking financial opportunities you never thought possible.

Remember, every financial decision is a step towards your future self. Your credit score is not a judgment—it’s an opportunity for growth.

FAQ

1. How often should I check my credit score?

- Check your credit report annually

- Use free credit monitoring services

- Review before major financial decisions

2. How long does it take to improve a credit score?

- Minor improvements: 3-6 months

- Significant changes: 1-2 years

- Depends on individual financial situations

3. Can I get a loan with a low credit score?

- Possible, but with higher interest rates

- Consider secured loans or credit-builder loans

- Work on improving score simultaneously

4. Do medical bills affect my credit score?

- Recent changes reduce medical debt impact

- Newer credit scoring models minimize medical debt weight

- Negotiate and verify medical bills

5. How do credit scores differ between countries?

- Scoring models vary internationally

- U.S. uses FICO and VantageScore

- Some countries have different credit reporting systems

Your financial future starts now. Embrace the journey, stay informed, and watch your credit score ranges transform from a limitation to a launching pad for success.

![]()