Credit cards are a powerful financial tool, but their impact on your credit score largely depends on how you use them. One of the most crucial factors in this relationship is understanding what is credit utilization.

Whether you’re building credit from scratch or aiming to boost your existing score, understanding and managing your credit utilization is essential for achieving your financial goals in 2025.

Skale Money Key Takeaways

- Credit utilization represents the amount of credit you’re using compared to your total available credit

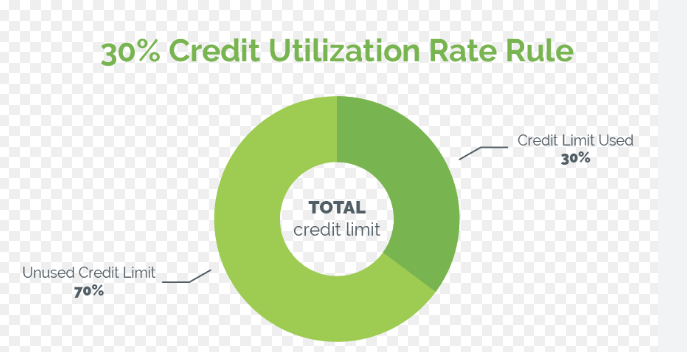

- Keeping your credit utilization below 30% is generally recommended, though lower rates often yield better credit scores

- Both individual card and overall credit utilization affect your credit score

- Credit utilization accounts for 30% of your FICO score, making it the second most important factor after payment history

- Strategic management of your credit utilization can significantly improve your credit score within a few billing cycles

Table of Contents

1. What is Credit Utilization and Why Does it Matter?

Credit utilization is the percentage of your available credit that you’re currently using. As one of the most influential factors in your credit score calculation, understanding what is credit utilization and how it works can make a significant difference in your financial health.

For example, if you have a credit card with a $10,000 limit and a balance of $3,000, your credit utilization ratio for that card is 30%. This percentage plays a crucial role in how lenders view your creditworthiness and financial responsibility.

- Credit reporting agencies use utilization to evaluate credit risk

- Higher utilization rates often indicate potential financial stress

- Lower utilization suggests responsible credit management

- Real-time utilization changes can impact credit scores quickly

Table: Credit Utilization Impact on Credit Score

| Utilization Rate | Potential Impact on Credit Score |

| 0-10% | Excellent – Best for credit score optimization |

| 11-30% | Good – Generally safe for maintaining good credit |

| 31-50% | Fair – May start to negatively impact scores |

| Above 50% | Poor – Likely to significantly lower credit scores |

2. How Credit Utilization is Calculated

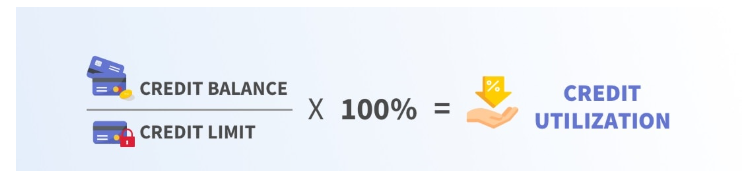

Understanding what is credit utilization calculation can help you better manage your credit cards.

The formula is straightforward: divide your current credit balance by your total credit limit, then multiply by 100 to get the percentage.

Let’s break down both individual and overall utilization calculations:

- Individual Card Formula: (Card Balance ÷ Card Limit) × 100

- Overall Utilization Formula: (Total Balances ÷ Total Credit Limits) × 100

- Credit bureaus track both metrics independently

- Some scoring models weigh overall utilization more heavily

For instance, if you have three credit cards: Card A: $2,000 balance on $5,000 limit (40% utilization) Card B: $500 balance on $3,000 limit (17% utilization) Card C: $1,000 balance on $7,000 limit (14% utilization) Your overall utilization would be: ($3,500 ÷ $15,000) × 100 = 23%

3. The Relationship Between Credit Utilization and Credit Scores

The connection between what is credit utilization and your credit score is direct and significant. Credit utilization accounts for approximately 30% of your FICO score, making it the second most important factor after payment history.

- Higher utilization typically leads to lower credit scores

- Score impacts can be seen as soon as new utilization rates are reported

- Different credit scoring models may weigh utilization differently

- Historical utilization patterns may influence score calculations

Most credit scoring models are designed to reward lower utilization rates, as they indicate responsible credit management and lower risk to lenders. Even small changes in utilization can have noticeable effects on your credit score.

4. Optimal Credit Utilization Rates

While the traditional advice suggests keeping utilization below 30%, recent data indicates that lower rates often result in better credit scores.

Understanding what is credit utilization’s optimal range can help you maximize your credit score.

Table: Optimal Utilization by Card Type

| Card Type | Recommended Utilization |

| Rewards Cards | 1-10% (to show activity while maintaining low utilization) |

| Business Cards | 10-20% (demonstrates business credit management) |

| Secured Cards | 20-30% (shows responsible usage while building credit) |

Industry experts increasingly recommend keeping utilization below 10% for the best possible credit scores. However, this needs to be balanced with practical usage and reward earning opportunities.

5. Strategies to Lower Credit Utilization

Managing what is credit utilization effectively requires a combination of strategic approaches and consistent monitoring. Here are proven strategies to maintain lower utilization rates:

- Make multiple payments per month to keep reported balances low

- Request credit limit increases every 6-12 months

- Time your payments before statement closing dates

- Consider balance transfer options for high-utilization cards

Remember that credit card companies typically report your balance to credit bureaus on your statement closing date, not your payment due date. Timing your payments before this date can help maintain lower reported utilization.

6. Common Credit Utilization Mistakes to Avoid

Understanding what is credit utilization also means knowing what practices can harm your credit score. Many consumers make these common mistakes without realizing their impact:

- Closing old credit cards (reduces total available credit)

- Making large purchases right before applying for loans

- Ignoring small balances on multiple cards

- Assuming utilization doesn’t matter if you pay in full

These mistakes can inadvertently increase your utilization rate and potentially damage your credit score, even if you’re making all payments on time.

7. Advanced Credit Utilization Techniques

For those seeking to optimize their credit scores, advanced understanding of what is credit utilization can lead to sophisticated management strategies:

- Strategic timing of credit card applications

- Rotating high-expense cards to distribute utilization

- Leveraging business credit cards for personal expenses

- Using secured cards to increase available credit

Remember that these advanced techniques require careful management and shouldn’t be attempted without a solid understanding of basic credit principles.

8. Credit Utilization in Special Circumstances

Different types of credit products and situations can affect how what is credit utilization applies to your credit profile:

- Business credit cards may not report to personal credit reports

- Authorized user accounts can impact your utilization ratio

- Secured credit cards typically have lower credit limits

- Store credit cards often have higher utilization rates

Understanding these special circumstances can help you make better decisions about credit applications and usage patterns.

9. Tools and Resources for Monitoring Credit Utilization

Effective management of what is credit utilization requires regular monitoring and adjustment. Modern tools make this process easier:

- Credit monitoring services provide utilization alerts

- Mobile banking apps show real-time balance information

- Credit card issuer tools calculate utilization automatically

- Personal finance apps track spending and utilization

These tools can help you maintain optimal utilization rates and respond quickly to any changes that might affect your credit score.

Conclusion

Understanding what is credit utilization and how to manage it effectively is crucial for maintaining a healthy credit score in 2025. By keeping your utilization low, monitoring your accounts regularly, and implementing the strategies outlined in this guide, you can maintain optimal credit utilization rates and improve your overall creditworthiness.

Remember that credit utilization is a dynamic factor that you can actively control. Unlike other credit score factors that take time to improve, changes in utilization can impact your score relatively quickly, making it a powerful tool for credit score management.

Frequently Asked Questions

Does paying in full every month affect credit utilization?

Yes, but what matters is the balance reported to credit bureaus, which typically happens on your statement closing date, not your payment due date.

How often is credit utilization updated?

Credit card issuers usually report to credit bureaus monthly, coinciding with your billing cycle.

Can you have 0% credit utilization?

Yes, but having a very small balance (1-2%) reported on one card might be better for your score than 0% across all cards.

Does requesting a credit limit increase hurt your score?

Soft pull requests typically don’t affect your score, but confirm with your issuer whether they’ll perform a hard credit check.

How does credit utilization affect mortgage applications?

Lenders often look at both current and historical utilization patterns when evaluating mortgage applications.

What’s the difference between statement balance and current balance for utilization?

Credit bureaus typically use the statement balance to calculate utilization, though some issuers may report current balances.

Expert Tips and Additional Resources

Financial experts recommend checking your credit utilization at least monthly and making adjustments as needed.

For the most accurate information about what is credit utilization and its impact on your credit score, consider consulting:

- Annual credit reports from annualcreditreport.com

- Credit scoring educational materials from FICO and VantageScore

- Your credit card issuer’s educational resources

- Credit counseling services for personalized advice

Remember that managing your credit utilization is an ongoing process that requires regular attention and adjustment. By staying informed and proactive, you can maintain optimal utilization rates and support your overall financial health.

![]()